Is the Trillion Dollar Coin a Dumb Idea or a Dumb Idea Whose Time Has Come?

I asked some actual economists

It’s hard to overstate how bad it will be if the US defaults on its debt. But let me try: If we default, the moon will explode and the ensuing fireball will incinerate heaven so that none of us can get in. Sharks will mate with rats, Christ will return to Earth and enter a polyamorous triad with Mark and Donnie Wahlberg, and the price of a Little Caesars pizza will go up for the first time in 30 years. Any attempt to access your bank account will be met with that creepy face from the Black Mirror “Shut Up and Dance” episode, and the only currencies that will be worth anything will be Dogecoin and blowjobs.

{kind=link}

I’m exaggerating, but only a bit.

We are, once again, facing a catastrophic default brought on by the debt ceiling. It’s an irritating ritual full of arcane rules that rolls around every few years against everyone’s wishes, much like the Winter Olympics. Republicans are insisting that the ceiling be raised using only Democratic votes. That’s annoying, but infinitely more annoying is that when Democrats tried to do that, Republicans blocked that, too.

The Treasury says that if we don’t raise the ceiling, we’ll run out of money on about October 18. That’s when all the moon exploding/shark-on-rat action would ensue (in non-hyperbolic terms: Plunging stock markets, unpaid soldiers, general global financial chaos). As it happens, there’s an incredible, unlikely, phenomenally-weird but not-impossible workaround to this chaos: The Treasury could mint a $1 trillion coin. Seriously. If you haven’t heard of this before: I’m not joking. It’s an absolutely Clown Town move, but since Clown Town is our primary residence these days, let’s put on a red nose, spray some seltzer down our pants, and give this idea the serious consideration it deserves.

As with most annoying congressional rules, the debt ceiling was created by accident long ago. In the 19th century, the Treasury had to get permission from Congress to issue debt. This was stupid, because it’s not like Treasury was blowing America’s money on whalebone corsets and nerve tonic; they were issuing debt to pay for things that Congress told them to pay for. Eventually, Congress said “you don’t have to come to us every time — just go ahead and issue debt up to X amount.” This only sort of solved the problem, but you have to cut people back then some slack — everyone in those days was suffering from mercury poisoning and a half dozen-odd mule kicks, so any action that’s not phenomenally stupid should probably be rounded up to “pretty good”.

In the 20th century, we started bumping up against the limit that Congress had set. This led to votes on raising the debt ceiling that were pro-forma, because everyone knew defaulting would be insane. Even if you loathe debt, trying to reign it in by having the country not pay its bills is idiotic. It's the equivalent of saying “I hate dandelions, and my solution is to napalm the entire neighborhood.”

But, about a decade ago, Republicans started threatening to napalm the neighborhood in order to force policy concessions out of Obama. This hostage-taking exercise has continued to today, except when Republicans control the government, because when Republicans are in power they don’t care about debt. And now comes the part of the column where I complain about the filibuster: There would be no issue right now if it weren’t for the filibuster. Democrats have the votes to raise the limit, except for the filibuster. I wonder if I’ll ever write an entire column without mentioning zoning or the filibuster.

Anyway: We have until the 18th to raise the cap. Republicans seem uninterested in negotiating, because a vote to raise the ceiling might result in a primary challenge from some weapons-grade idiot who would hold that vote against them. If push came to shove, they’d probably at least not block a Democratic vote at the last possible minute, but that’s a dangerous game of chicken and encourages more of this crap in the future.

It’s clear what Republicans want: They want Democrats to use the reconciliation process to raise the cap. If you feel a burning need to know the specifics of how reconciliation works in this instance, here’s that, but more importantly here’s a directory of therapists who might be able to treat your affliction. The upshot is that reconciliation can be used to raise the debt ceiling, and it can be done without damaging the major spending bill that Democrats are trying to pass. BUT, it might or might not be possible to do it by October 18th.

Republicans want Democrats to go through reconciliation because the process will force them to cast bunch of unpopular votes. Part of the reconciliation process is what’s called a “vote-a-rama” which is a portmanteau of “vote” and “rectal enema”. The goal of a vote-a-rama is nominally to propose amendments, but actually to force the other party to cast unpopular votes that can be used in campaign commercials. The way it works is: You propose an amendment to, say, protect seniors from boa constrictor attacks and add the phrase “four total gaywads” to Mount Rushmore. The amendment obviously fails, and then you run an add saying “Senator X voted against a bill to keep seniors from being swallowed by giant snakes.”1

I agree with this take that argues that Democrats are way, way too concerned about these ads. The connection between a member of Congress’ actual voting record and how that record is portrayed in campaign ads is already almost nonexistent. It’s impossible to be in Congress for any length of time without casting some weird procedural vote that would look bad when paired with grainy footage and ominous music. Besides, the type of voter who falls for those ads can probably be convinced by the footage and music alone; you could probably say “Tammy Duckworth keeps her bread in the refrigerator” and the dullest among us will think “Wow, Tammy Duckworth is basically Hitler.”

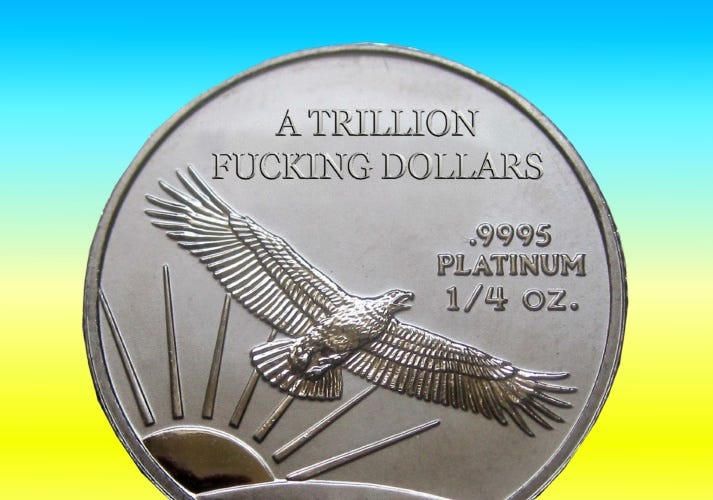

The fact that Republicans are threatening to melt down the global economy in the hope of leveraging a few cheesy campaign commercial throws me into full “fuck everything” mode. Which brings us to the trillion dollar coin. Continuing the theme of “Congress doing things completely by accident,” a 1997 bill empowered the Treasury to mint platinum coins. This bill had nothing whatsoever to do with the debt ceiling. It was just a bill to let the Treasury make those commemorative coins that you see advertised during baseball games and airings of Saving Private Ryan. You know the ones — they feature iconic moments in American history, such as:

Or:

Or:

Here’s the thing about that bill: It didn’t limit how much the Treasury can declare a coin to be worth. So — without getting deep into the details of the relationship between the Treasury and the Federal Reserve and how debt becomes spendable cash — this is possible: The Treasury can deposit the coin at the Fed. The Treasury can then draw down against the value of the coin, eliminating the need for new debt (for a long time, anyway). Because the mechanics of how the Fed would create this money are similar to what they’d do under ordinary circumstances, there’s basically no difference in inflationary impact between the coin and business as usual.

Would this be legal? Probably. Is it proper? Oh FUCK no — do you even need to ask that? This is some shady shit — it’s the monetary policy equivalent of selling expired meat out of a van. In fact, one of the arguments in favor of the coin is that everyone will know it’s just a gimmick to get around a dumb rule — it’s not actual money. But it would be an unprecedented move, so let’s run through some of the pros and cons.

PROS:

A big fucking coin is cool. I’m sure we can all agree: The coin should be physically large. You don’t make a trillion dollar coin and have it be some weensie little nothing that someone could accidentally put in a washing machine. No: You need a big, heavy, dinner plate of a coin, I’m thinking about ten inches in diameter, so that Janet Yellen can put it on a chain and wear it around her neck like Flavor Flav’s clock.

Heist movies. Once you’ve got a trillion dollar coin deposited at the Fed, the script writes itself. I’m thinking Michael B. Jordan in the Danny Ocean role, with Andrew Garfield as the inside guy, Kyle Mooney as the hacker/comic relief, and Chuck Norris as Jerome Powell. Yeah: I could picture watching that on a plane and thinking it was fine.

Republicans would see that Democrats can fight stupid with stupid. The obvious problem here is that Republicans know that if they act like babies, the grown-up party will find a way to do the responsible thing. They’d surely act differently if Democrats were to really amp up the crazy and dumb. Maybe this entire era of politics could have been avoided if Obama had loudly shit his pants at his first inaugural, sat down in it, and said “I’m just gettin' warmed up, ya bunch-a dildos.” That would have really sent a message.

CONS:

People on Twitter like it. I’m instantly skeptical.

It's shenanigans. Readers of this blog know that I am against shenanigans, tomfoolery, and falderal. I think policy should be made on purpose and according to a process, not by some weird game of Calvinball that always seems to reward whoever has the fewest scruples. The only reason the coin is even worth talking about is because default is so terrible.

It’s so goofy that it might seriously disrupt the dollar’s value. At the risk of getting all stoned-college-freshman on you: Isn’t it weird that money is just, like…whatever we say it is? And, yes, 18 year-old me: It is weird, but the fact that we’ve managed to basically agree on what a dollar is worth is to our great mutual benefit. Minting a trillion-dollar coin would highlight the fact that the dollar — which happens to be the world’s top reserve currency — is backed by a government that’s resorting to schemes literally stolen from a Simpson’s episode. It could sew chaos. And I’m sure anyone sitting on a few dozen Bitcoin is thinking “yes, let’s do that!” But it might not be so good for the rest of us.

So…do the pros outweigh the cons? Here’s where I need to admit my limitations; I’m not an economist. I studied economics in school, I try to keep up on it, but truthfully, I’m an economist in the same way George Costanza was an architect. The accurate way to phrase it is that I’m good at economics for a standup comic, which is like being an amazing tap dancer for a botanist.

So, I polled some actual economists: Would it be worse to hit the debt ceiling or to mint the coin? I sent that poll to economists at ten top universities,2 and, incredibly, some responded. Here are the results:

Thanks for nothing, eggheads! It reminds me of that Harry Truman quote about how he’d like a one-handed economist, so that they wouldn’t always say “on the other hand.” Which, of course, was a more-clever phrasing of his original statement: “Economists blow.” At any rate: A sincere “thank you” to the economists who stopped doing their jobs to respond to my stupid poll, which ultimately resolved nothing.

If hitting the debt ceiling is imminent, we have unusual options available to use other than minting the coin. Dylan Matthews does an excellent writeup here; the options are:

Invoke the 14th Amendment. The 14th Amendment contains a clause saying that the public debt of the United States “shall not be questioned.” Shall not even be fucking questioned — don’t even think “is this T-Bill going to pay out?” I shouldn’t have even typed that. And you shouldn’t have read it! Burn your computer — we’re now in a criminal conspiracy together!

Is this legal argument any good? Well, the Obama administration said “no”, but like all constitutional questions, is exists in a Schrodinger’s cat state until a court rules on it. But, in this case, it might be hard to get a ruling. Truthfully, the main function of all of these unconventional options is to buy time for Congress to make the debt ceiling irrelevant.

Declare ignoring the debt ceiling to be the “least unconstitutional” option. Congress has given the executive branch three mandates: 1) Spend what we tell you to spend; 2) Tax what we tell you to tax; and 3) Issue only as much debt as we authorize. When the debt ceiling is hit, the president can’t do all three at once. So, since he has to ignore something, he should ignore the debt ceiling (and then prepare to be sued). Some fancy-pants law professors have made the case for doing this. Of course, if my poll about the coin is any guide, it’s probably possible to dig up an equal number of eggheads who would argue the exact opposite opinion, so take that analysis with a grain of salt.

Issue “quasi-debt”. The debt ceiling applies to Treasury Bills. But what if we issued…Schmeasury Bills? Could those be a thing? This has been tried enough at the state and local level that these securities have a name: “Special purpose entities.” And any comedy fan can guess what’s coming next:

I think it’s past time to do away with the debt ceiling. If the only way to do it is to go through the reconciliation/vota-a-rama process, then I think Democrats should do that. The fix should be permanent, and personally, I like the proposal outlined by Georgetown law professor David Super here.

But what if it can’t get done in time? Well, then I think you have to resort to either the coin, the 14th Amendment, the Schmeasury Bills, or the “least unconstitutional” argument. Personally, I’m leaning towards the “least unconstitutional” argument; it seems less likely to rattle financial markets than the coin or Schmeasury Bills, and seems more legal than invoking the 14th Amendment. But I could be talked into one of the other choices; unlike with economics, I don’t even pretend to be a legal scholar.

I think one thing people like about the coin is the sheer fuckery of it. A trillion dollar coin is nuts, and the idea of a half-joking scheme floated by a blogger averting a financial crisis is a fantastic narrative. It’s an idea whose wackiness seems right for the moment, a true case of fighting stupidity with stupidity. I completely get that. But, as previously stated: I am against tomfoolery. I don’t like the flippant, Twitter-borne, nihilistic approach to politics. I think maybe five percent of Trump voters voted for him out of sheer boredom — they wanted chaos, and God damn did he ever deliver. I’d like to go in the other direction. So, while default should be out of the question, and I’m open to anything that avoids default up to and including the coin, I’d strongly prefer a workaround that isn’t metaphorically wearing a diaper and slathering itself with jam as it runs for Mayor of Clown Town.

***POLL FOR NEXT WEEK***

I'd like the next column to be about...

1. How the only thing worse than "corporate media" might be "populist media" [VOTE FOR THIS]

2. How vaccine mandates are working [VOTE FOR THIS]

3. How calling someone "stupid" is rightly verboten in politics, but it sometimes makes explaining a phenomenon difficult [VOTE FOR THIS]

I used an example for comedic effect, but what you’d actually do is pick something that’s a wedge issue for the other party. So, for example, you might try an amendment that’s extremely pro-coal, and most Democrats would hate that, but if Joe Manchin keeps solidarity with other Democrats and votes “no” (because there’s often pressure to vote down all amendments), then you can use that in a campaign ad.

Here’s my highly unscientific method: I googled “top economics departments” and found this list. I went down the list looking for departments that have their faculty e-mails on one page; I eliminated any school where I had to click on a professor’s profile in order to get their e-mail. I did this until I had ten schools, which ended up being Harvard, Stanford, Columbia, Brown, Yale, Penn, UC San Diego, Northwestern, Michigan, and Georgetown. I emailed the poll to every professor from those schools who had their e-mail publicly listed and waited about a day for replies. FWIW, I think my e-mail ended up hitting some sort of spam filter, because I got those 21 replies very quickly and haven’t gotten one since.

You should only poll economists who understand that taxing capital gains at the same rate as labor is not a Bad Thing. My guess: those economists prefer the Coin.

Coin, Coin, Coin!

Calvinball!

To quote James Bond in Road to Perdition, its all so fuckin hysterical.